School board seeks outside legal counsel for response to grand jury report

–The Paso Robles Joint Unified School District Board of Trustees met for four hours Saturday morning to craft a response to the San Luis Obispo County Grand Jury Report. The report, “Paso Robles School District: A Cautionary Tale”, criticizes the previous board for financial mismanagement during the tenure of former Superintendent Chris Williams and his board of trustees.

–Read the entire grand jury report below the story–

The board agreed 5-1 to hire independent legal counsel to help craft its response. Board President Chris Arend voted no, Trustee Lance Gannon did not attend the meeting. Two former board members called in to the meeting to address their actions while serving on the board. Joel Peterson and Joan Summers called into the special meeting to defend the actions of the previous board.

The board then went point-by-point through PRJUSD Board President Chris Arend’s draft response to Grand Jury Presiding Judge Jacquelyn H. Duffy. Their discussion included issues such as conflicts of interest, nepotism, and cronyism, which the Grand Jury said in their report led to teacher morale issues which were documented in two union-sponsored surveys. The current board questioned two trustees who served during that time: Chris Bausch and Tim Gearhart. Those two reflected on the consensus of the board during the years between 2014 and 2018 to help the current board formulate a response to the grand jury.

Superintendent Curt Dubost at PRJUSD board meeting

One of the more serious issues was the $235,000 severance pay awarded to Williams when he resigned. The grand jury wrote, “The superintendent was not eligible for a severance package when he resigned. However, the board extended a negotiated settlement without obligation to do so.” The board discussed Arend’s draft response to the Grand Jury’s statement. Arend reminded trustees during the meeting that he took part in a later meeting with Williams and his attorney which resulted in a “claw-back” almost half of that money.

The board agreed with most of the findings of the grand jury, but disagreed partially with some. The discussion proceeded slowly, and ended at 12:15 p.m. The board agreed to meet Tuesday, Feb. 2nd at 4 p.m. to continue the discussion of the report, so they can send a response back to the Grand Jury, which is required by mid-February.

The entire special meeting is available to watch on YouTube. Read the entire grand jury report below:

PASO ROBLES SCHOOL DISTRICT: A CAUTIONARY TALE

Paso Robles Joint Unified School District finds itself in another financial crisis, the second since 2012. This report looks at failures in leadership and management that precipitated the recent crisis, and provides a detailed illustration of how a school district can inadvertently fail its students and the community it serves.

SUMMARY

Between 2015 and 2018 financial problems resurfaced within the Paso Robles Joint Unified School District (PRJUSD). As in 2012, they became subject to a Grand Jury investigation. This is a three-part Grand Jury report examining PRJUSD. The trilogy of reports, School District Leadership, District Reserve Management and The Aquatic Complex, is intended to highlight how people, systems, and institutions fell short in their obligations to its citizens.

This report was self-generated, prompted by news reports, in accordance with government guidelines for the Grand Jury. As a result of the San Luis Obispo Grand Jury (SLOGJ) investigation it became clear that there were serious shortcomings in both district and county leadership as well as financial management.

The chapter on leadership focuses on three key elements: the district superintendent and administration, the School Board of Trustees and the County Board of Education. This report highlights significant failures by these groups in managing budgets, controlling expenditures, and providing the oversight necessary for the health of any school district.

The chapter on financial reserve management provides an audit trail documenting the ill-advised actions, unbudgeted expenditures by the superintendent, and lack of proper oversight by the Board of Trustees. This resulted in a reduction of financial reserves from a comfortable 10% of budget to an extremely precarious, less than 1% of budget, in a four-year period. As a result, for the second time in less than seven years, the district was placed under county financial control.

The third chapter explores the circumstances surrounding the planning and execution of an aquatics complex intended to be constructed for the benefit of the Paso Robles school district and the community. The grand jury chose to highlight this as an example of what might be considered extremely poor judgment on the part of the parties involved. As of the date of this report, there is no clear plan or path forward for the construction of a complex. However, to date, $1.5 million of Measure M funds have been expended. This includes the poorly timed purchase of modular stainless steel components for the vinyl-lined pools that have now been paid for and placed in storage for over two years.

The PRJUSD administration, the Board of Trustees and the County Board of Education failed to fulfill their obligations, learn from previous mistakes, and balance vision with pragmatism, ultimately offering a cautionary tale and guidance for school districts throughout the county.

METHOD/PROCEDURE

The Grand Jury conducted twelve interviews, conducted a county-wide survey of the ten primary school districts (Appendix A), reviewed hundreds of documents (Appendix B), attended numerous School Board meetings and finally, jurors toured Paso Robles High facilities for the purposes of completing this report.

CHAPTER 1 – SCHOOL DISTRICT LEADERSHIP

PURPOSE

The purpose of this chapter is to report on the investigation into the impact of leadership failures at three levels: the District Superintendent’s Office, the PRJUSD Board of Trustees, and the County Office of Education. This chapter will help highlight the complexity of school administration and the need for well-trained, elected officials to be knowledgeable and engaged. The expectation is that everyone who cares about the education of our youth will read this and look at how education is being administered and by whom. With acknowledgment and understanding of personal and systematic shortcomings, other districts can benefit by learning these lessons.

NARRATIVE

Failure at three levels of leadership: the District Superintendent, the District Trustees and San Luis Obispo County Office of Education (SLOCOE), contributed to the problems being addressed in this report. In order to help other districts in SLO County avoid future issues it is critical that each entity is examined.

The Role of the Superintendent

The superintendent of a school district oversees the daily operations and the long-range planning of their district. The primary responsibilities of a superintendent are to supervise school principals and district staff, work with school board members, develop curriculum and manage fiscal operations. School District Superintendent standards are documented at: (Link)

After the unexpected retirement of the long-term district superintendent in June 2014, a new permanent superintendent was hired in August 2014. At that time the financial reserves, the financial safety net for a school system, were strong. After the 2012 crisis the reserves were built back up to as high as 10% of the annual budget, an amount in excess of six million dollars.

The newly hired superintendent presented the community with a one-hundred-day plan, which would bring new programs, additional staff, and improved facilities to Paso Robles schools. He desired to revitalize educational efforts within the district and attract more students to the district, which would generate more funding. The Visual and Performing Arts Program and enhanced athletic programs contributed to drawing in new students over the next few years.

While the objectives were good, the methodologies for achieving the objectives were problematic. Budget management was hampered by lack of institutional memory, significant personnel turnover among Chief Business Officers (CBO) as well as Financial Managers, and failure to use the tools available to maintain good financial accounting. During the four-year tenure of the superintendent, there were four different CBOs in PRJUSD. There were also four different financial managers who subsequently left in that same period. Twice the superintendent himself was acting Chief Business Officer, once for two months and later a four-month period. Beyond lacking the experience for this role, it left a serious gap in accountability with no systems for checks and balances.

Based on interviews and records it appears that the role of the primary business officer in Paso Robles district was a stressful one and the turnover only helped to compound mistakes made over time. The turnover did not allow for smooth transitions, the opportunity to learn from predecessors, or to share lessons learned. There were also problems with the utilization of the Quintessential School System (QSS), the automated finance program used by California state schools for maintaining accurate budgets, and issues with the development of new annual budgets.

The addition of new positions and related hiring practices were also problematic. In a four-year period, from 2015 to 2018, 25.9 (full-time equivalent, FTE) previously unbudgeted administrative positions, were added within the district. Some of the positions were reclassifications from credentialed to administrative posts requiring replacement of the original vacated positions. Others were new positions not critical to the operation of the district office, including a District Communications Director and District Athletic Director. These staffing increases were made without consideration of the comprehensive cost including salary, benefits and pension plan and their ultimate impact on the budget. The superintendent appeared to rely on a one-time financial windfall from the state to fund these new positions without consideration for the sustainability of long-term budget requirements. This had the effect of depleting the reserves. . Since the departure of that superintendent, the overall number of district administrators has been reduced by 17.2 FTE.

Additionally, perceptions that long-term employees were being pushed out in favor of new employees, who were perceived to be more favorable to the superintendent and his plan for the district, caused distrust within the community and negatively affected staff morale. This was documented in teacher morale surveys, initiated by the teacher’s union, taken twice, one in 2018 and again in 2019. The results of these surveys were eventually independently published.

When the County Superintendent of Schools identified the onset of a financial crisis, written warnings were sent to the superintendent and president of the board. These written warnings were not passed on to other board members. As a result, the trustees were unaware of early warnings from SLOCOE. Eventually SLOCOE sent letters to all board members but they failed to take effective corrective action. Once the reserves fell below the mandated 3%, as they had in 2012, the County Superintendent was required by law to assign a monitor to address all the fiscal problems.

Eventually, the leadership problems came to a head. With the election of new members to the Board of Trustees in November of 2018, there was the recognition that the fiscal problem was extremely serious. A number of other concerns were also being raised and the superintendent resigned in December 2018. The superintendent negotiated a lucrative severance package as a condition of his resignation. According to the SLOCOE, the superintendent did not meet the requirements of his contract that entitled him to any severance package. However, the resignation was accepted and remunerated by the outgoing Board of Trustees, three of whom had not been re- elected, in a six-to-one vote for approval. As the three new members assumed their duties the board rescinded the outgoing board agreement. The SLOCOE monitor, who was not part of the first negotiation, though she should have been, would not approve the original agreement. The County Superintendent eventually helped negotiate a new agreement with a smaller settlement and with terms that saved the cost of a protracted lawsuit.

As part of our survey of the ten school districts in the county, SLOGJ asked what qualifications are needed for a Superintendent. The results of that survey are listed in Appendix A.

The Role of the District Board of Trustees

Citizens of Paso Robles elect seven trustees to serve as overseers of all school district operations and set policies that affect students in their schools. The board is tasked with setting the vision and goals for the district, and holds the district accountable for results. Theirs is a fiduciary and guidance responsibility to voters and taxpayers in the school district and the state. The California School Board Association (CSBA) offers detailed professional governance standards (Link)

School Board Trustees are citizens within the district who should act as advocates of strong educational programs and well-managed schools. Unfortunately, elected officials are not required to attend training programs before taking on the serious and complex duties of overseeing the operation of their school district. Based on interviews during our investigation with former and current Trustees of the School Board, not all members availed themselves of training opportunities necessary to oversee the operational systems used for managing multi-million dollar budgets. Such training is readily available from the County Office of Education, as well as School Trustee conferences. The SLOGJ surveyed the 10 school districts in the county to assess their Trustees training policies and procedures. The results of that survey are listed in Appendix A.

Financial oversight is a critical piece of any school district success. In the case of PRJUSD it would appear that trustees failed to practice due-diligence or independent verification of the financial information provided by the District Office before making critical financial decisions. In some cases the information provided was inaccurate or incomplete and led to decisions that had a negative impact on the financial health of the district.

Trustees have access to all district employees, and auditors. They routinely visit schools, participate in assemblies and school functions, and meet with district staff as a part of their Trustee duties. During the years in question, the Trustees were discouraged from performing these functions, which adversely impacted their ability to fulfill their obligations. Trustees also have access to legal advisors. Legal advisors are present at Board meetings when required by law. In Paso Robles there were reported violations of the Brown Act committed during Board of Trustee meetings when counsel was not present.

Trustees are given agendas and packets of related information in advance of each School Board meeting. It is their responsibility to digest this information and be ready to make decisions at subsequent meetings. In the time of the administration discussed, the packets went out on Friday for a meeting to be held the following Tuesday. They now go out on Thursday. Sometimes these packets have lengthy agendas requiring review of hundreds of pages of related documents, such as complex budget spread sheets, proposal documents and confidential personnel materials.

Through our investigation it appears that the desire to support the programs promoted by the new superintendent influenced the judgment of many on the board resulting in financial oversight being compromised. As a consequence, the financial reserves fell below the State mandated levels and forced the SLOCOE to assign a financial monitor to help restore fiscal stability.

Trustees approved new positions, purchased a million-dollar pool for a proposed aquatic complex without a completed construction plan and accurate construction estimates, and brought in new academic, athletic and student service programs, all before they realized they didn’t have the money to pay for them or sustain the long term costs. Board members relied on information coming from the superintendent and his direct reports and either did not bother to verify it or had no means to verify the information. As a result, a majority of the trustees routinely approved expenditures not supported by the budget.

Conflict of interest might have also played a role in the relationship between Board Members and the District Superintendent’s staff. There were circumstances where Board Members had family members who were employed by the District, jeopardizing the “arms-length” relationship preferred in such situations. This resulted in accusations of preferential treatment being given to certain employees.

In our survey of the ten school districts in the county, SLOGJ asked about the responsibilities, guidelines and training for Trustees. The results of that survey are listed in Appendix A.

The Role of the County Office of Education

According to a publication titled Statutory Functions of County Boards of Education & County Superintendents of Schools, the County Superintendent is responsible to work directly with the school districts in the county to provide guidance for their operation. A critical component of their job is to maintain responsibility for the fiscal oversight of each school district in their county. The passage of Assembly Bill 1200, in 1991, gave the county superintendent additional powers to enforce sound budgeting to ensure the fiscal integrity of the districts.

The County Office of Education got involved with Paso Robles during the 2012 financial crisis. They intervened when the reserves fell below the mandated 3% of the total budget and assigned a monitor to assist the board and the superintendent to restore reserves back to their mandatory levels. In a matter of one year the PRJUSD was fiscally sound, and the monitor was removed until deficit spending from 2015 to 2018 caused the reserves to fall below state-mandated levels. As a result, it became necessary for the district to allocate funds from their reserves to maintain these programs. The district ended up falling into a qualified approval status a second time.

As these issues surfaced and came to the attention of SLOCOE, through scheduled budget reviews, the County Superintendent of Schools and the Assistant Superintendent for Budgets and Finance wrote letters to the PRJUSD Superintendent and the President of the Trustees to note their concerns over budget conditions. The district took no effective corrective action. When it became apparent that the Trustee President and the Superintendent failed to pass on the concerns of the County Superintendent, the SLOCOE reached out directly to the board. Even so, conditions continued to deteriorate, forcing the County Superintendent’s Office to intervene directly and reinstate the monitor to bring the budget back to compliance.

CONCLUSIONS

The financial problems that developed at the Paso Robles Joint Unified School District were a result of the actions of three groups charged with school system oversight. Their collective failures to control or report on excessive expenditures created a fiscal crisis that will take time and hard work to resolve. The previous superintendent’s leadership is responsible for overestimating income and not controlling spending. Under his administration the constant turnover in business and financial staff caused mismanagement in monitoring finances and budgets. The Trustees had hired a superintendent with a new direction and vision with the hope to revitalize their district. Unfortunately, the available funding failed to support the new vision. Despite that fact, the trustees approved expenditures in excess of available funds without sufficient questioning. And finally,

the limitations in the SLOCOE oversight procedures prevented the County from officially intervening in the district’s deficit spending pattern. Despite repeated warnings communicated to the superintendent and the Board President, no corrective action was taken. It was later determined that the communications from the County were never forwarded to the other trustees who remained unaware of the financial crisis on the horizon. On the other hand, the trustees are required to practice due diligence, which they failed to do.

This trifecta of abdication or dereliction of duties, mismanagement and leadership failure was evident in hearing from individuals and reviewing the documents requested by the Grand Jury in search for the truth of just what happened in Paso Robles. The circle of blame is a large one that offers a cautionary tale from which every school district can benefit.

CHAPTER 2 –RESERVE MISMANAGEMENT

PURPOSE

This chapter of the report seeks to summarize the financial conditions and actions that lead to a significant depletion of the reserves of the Paso Robles Joint Unified School District (PRJUSD) for the second time in a decade. The Grand Jury report will seek to provide answers to what happened to the PRJUSD’s reserves from the 2014/15 school year budget through the 2018/19 budget.

BACKGROUND

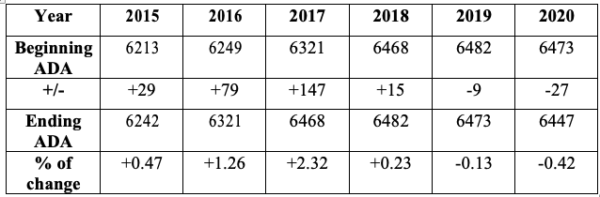

The State of California, within its educational regulations, mandates that each California School District maintain a budget reserve. A financial reserve is established to provide contingency funds in the event that unplanned expenditures and unexpected reductions in revenue have an adverse impact on the school district’s budget. The vast majority of funding made available to the PRJUSD comes from the State of California and is based upon the district’s reported Average Daily Attendance (ADA). As expected, the reported ADA can fluctuate over the course of a school year impacting funding provided by the state. A district’s ADA is projected at the beginning of the year and reconciled at the end of the year. Reserves can serve the purpose of closing the gap between differences in projected and actual ADA.

NARRATIVE

What happened to the reserves?

In August of 2014, a new superintendent for the PRJUSD was hired by the Board of Trustees with a promise to revitalize the school district with exciting new programs that were outlined in his one hundred-day plan. In the first fiscal year of his term in office (2014/15), the PRJUSD’s budget reserves stood at 10.4% or $6,051,333. This was a fiscally healthy amount and exceeded the mandatory (3%) requirement for reserves.

School reserves are a ‘rainy day fund’ that exists as part of the multi-million-dollar school budget. Reserves should be thought of as undesignated funds to be used for an emergency or unforeseen expenses. These reserves are held in two separate accounts, with a portion of the accounts being held in the district’s general fund and the district’s building fund. When reserves drop below the mandated minimum of 3%, the County Board of Education is required to assign a financial monitor to oversee and assist in re-establishing reserves at an acceptable level. The following chart shows how reserves declined by fiscal year.

Between 2015 and 2019, nearly six million dollars in reserve funds were depleted. This was primarily due to administrative and accounting errors, poor fiscal planning, and improper management guidance.

The following seven areas have been identified as the problem areas that caused the majority of unbudgeted spending which depleted the reserves.

1. MISCALCULATED AVERAGE DAILY ATTENDANCE

The State of California pays each school from $7,000 to $9,000 per student based on a complex formula calculated from Average Daily Attendance (ADA) records. During the 2016/17 and 2017/18 fiscal years, the PRJUSD input their ADA incorrectly. This error was based on untrained personnel using an incorrect formula to report and calculate attendance. The mistake was corrected when the auditors noted that there was an over counting error. The net effect was an unplanned expense to the budget of $1,014,024 that was taken from reserves. This ADA calculation formula has been abandoned and new management is on track with the standard accepted practice for ADA calculation.

2. IMPROPER TRANSPORTATION COST CALCULATIONS

Student transportation costs for the PRJUSD are a significant expense. The nature of the district required 12 unique routes to rural and urban areas. The shortage of drivers, as well as the increased cost of labor and maintenance, was not properly budgeted. As a result, a seven-figure unplanned expense against the transportation budget resulted in another reduction to the reserves. Current management is addressing these transportation issues in new and creative ways that previous management did not consider.

3. DISALLOWED FOOD SERVICE EXPENDITURES

The Culinary Academy is a vocational training school that exists as part of the PRJUSD and provides food service to all the district schools. In the 2017/18 school year there was an error in accounting for the number of students eligible for reduced cost or free meals. This error was similar to the ADA error discovered by auditors. The academy leader, at the time, submitted expenses that were ultimately disallowed by the auditors and rejected by the state. These expenses were unplanned and were paid from school district reserves. The Culinary Academy is now under new management.

4. ERRORS IN ACCOUNTS PAYABLE ADMINISTRATION

The PRJUSD had two major accounts payable errors. For two years, fiscal 2013/14 and 2014/15, payables for insurance coverage were thought to be the responsibility of the San Luis Obispo County Office of Education. This coverage was, in fact, determined to be the responsibility of the district. This resulted in a $930,089 expense to the district, which impacted the reserves.

5. INSUFFICIENT PLANNING FOR PENSION AND SALARY INCREASES

Pension demands from CalPERS and CalSTRS have been increasing for several years. The following table, from PRJUSD audits, show the effect of increased pension costs, the yearly deficit, and pension increases for the last six years. The State of California has used surplus funds in the last two years to decrease the burden and assist districts to fund their retirement commitment.

In the fiscal year 2015/16, pension costs represented 5.8% of the PRJUSD’s budget. In the 2018/19 budget, the requirements to pay pensions increased to 12.4%. In three years, the pension percentage of the fiscal 2018/19 budget of $85 million climbed 6.6% or roughly $6 million.

In addition to pension support, there were salary increases of nearly 20% that occurred between 2015 and 2019. These increases were negotiated and were required by contract.

The District Superintendent and the Board of Trustees did not properly plan for pension and salary increases. The lack of long-range planning and accountability by the administration resulted in loss of reserves.

6. UNPLANNED AND UNBUDGETED LEGAL SETTLEMENTS AND FEES

Three lawsuits were filed and corresponding legal fees were paid during this period. There was no provision at the time within the budget for the potential loss from these lawsuits. These types of losses to the school district are normally paid by insurance and reserve funds.

7. FAILURE TO CONSIDER TRUE COSTS OF NEW PROGRAMS AND HEADCOUNT

During the 2015/16 fiscal year, several new programs to help boost attendance at Paso Robles schools were initiated. This included a Visual and Performing Arts Program (VAPA) as well as elementary and middle school athletic programs. Staff to support these programs and other staff increases, equaling 25.9 full-time equivalent positions, dramatically increased payroll and was not properly accounted for in the Quintessential School Service budget program.

Under the new management of the PRJUSD, and the San Luis Obispo County Office of Education appointed monitor, many non-essential positions have been eliminated or reclassified. In 2019/20 a new round of certified and classified layoffs and other changes to the PRJUSD were announced showing the long-term impact of 2015/16 decisions. At the time of this report, primarily as a result of savings in operational cost from virtual school attendance, the reserves have been replenished to a level where the county monitor could be withdrawn.

Though the majority of reserve losses can be attributed to these seven categories, it is important to note that there are other expenditures that exceeded the budget that are not detailed in this report.

Why did this mismanagement occur?

In retrospect, there was a series of administrative issues, lack of proper management oversight, bad management decisions, and a failure to question leadership when it was necessary. All of the above point to the reasons for the failure to maintain reserves at the proper level.

The PRJUSD manages its budget with a tool that many other districts utilize, which is called the Quintessential School System (QSS). The QSS program is, in effect, the systematic tool that provides the school district with a detailed financial budget and means to manage it.

The current PRJUSD budget is 163 pages long with over 1,500 detailed financial activities, including labor costs, overhead, supplies, operating and facility costs, as well as the reserves, which make up the district budget. The sum of all line items in the QSS system is, in effect, the school district’s budget.

Each line item is allocated a budget. Expenditures are tracked against it throughout the school year. The line item budgets are grouped under department managers who are accountable for their financial performance. The QSS has an effective ‘check and balance’ feature that prevents expenditures beyond the budget line allocation. For example, assume the line item budget for pencils is $12,000 and someone submits a requisition to purchase $14,000 worth of pencils; the QSS system will not allow the requisition to be placed. The pencils line item must be increased to $14,000 for the requisition to be approved.

As a general rule, the individual department manager has authorization to increase the budget by moving one budgeted line item to another line item under his or her control. If a manager does not have additional money in their budget under his or her control, then a request must be submitted to the Chief Business Officer (CBO) to move additional budgeted money from either another department or from financial reserves.

The system prevents expenditures that exceed the budgeted line item. If utilized as intended, the QSS system can provide adequate financial oversight. In the time period from 2015/16 to the 2018/19 time periods, it was unclear who had the authority to make these budget adjustments and what financial oversight was provided to insure financial stability.

Additionally, the QSS system is complex and the administrative managers appeared to override the safeguards built into the system. The Grand Jury was not made aware of standard reports being provided to the trustees to allow them to properly manage the spending process during the period in question. Some reports to control the budget were done more on an ad hoc basis. The Grand Jury did not see, in its extensive investigation, the kind of in-depth analysis that should have be done on such a large, complex budget to provide adequate control.

Control of the budget process was ultimately in the hands of the CBO. During the period in which the reserves were depleted, there were four different CBOs including the superintendent himself. A lack of management oversight, at times, allowed a freedom to overspend within technical guidelines. Under normal circumstances, this behavior would have been questioned by a vigilant CBO.

The Culinary Institute manager had some serious issues handled by the San Luis Obispo District Attorney’s Office not reviewed by the Grand Jury. Billing for free or reduced cost meals resulted in a disallowed reimbursement by the State.

CONCLUSION

At the beginning of 2015, financial reserves were at a very healthy 10.4% of the PRJUSD budget. This provided the new district superintendent a solid financial cushion. The superintendent utilized the positive financial reserves to fund new programs, which he presented in his one hundred-day plan. The cost of these programs over this three-year period contributed to the reduction of reserves from 10.4% to 0.3% (below the mandated 3.0%).

There was strong evidence of mismanagement in overseeing important business areas such as ADA calculations, the culinary academy budgets, transportation, payroll and pensions. The extremely high rate of turnover among fiscal managers (eight people in a four year period) caused a vacuum in the financial management of the district.

In retrospect the PRJUSD between 2014 and 2018, the Superintendent had a grand vision on how to improve the district. His decision to deliver this grand plan, regardless of the financial impact, cost the school district millions of dollars in reduced financial reserves. To all concerned, the County Office of Education, the PRJUSD Superintendent, the Board of Trustees, and to the electorate, this should be a lesson taken seriously.

CHAPTER 3 – THE AQUATICS COMPLEX

PURPOSE

The purpose of the report is to illustrate how the administration of the Paso Robles Joint Unified School District (PRJUSD) erred and created financial blunders that impacted the entire district operation. The Grand Jury (SLOGJ) believes that nothing illustrates these failures better than the example of the Aquatic Complex plan, which to date, is not close to being constructed.

NARRATIVE

In 2015 the new superintendent wanted to produce a new facilities master plan (FMP) anticipating a significant increase in school enrollment and other factors. This increase would require modifications to existing facilities and construction of new facilities to support anticipated growth. The Dolinka Group, commissioned by the superintendent, had estimated an annual student increase of 2.19% from current levels on a continuing basis. Some increase happened in years 2015 to 2018 and has declined since. In only one year did the increase approach the 2.19% that was projected.

The PMSM Architectural Firm was hired in 2016 to study every school, meet with teachers, parents and staff to determine the current state of the infrastructure, and look to the future for the changing educational needs. In April 2016, the Board of Trustees was presented with a completed plan that was used to estimate the costs for a potential bond issue to fund the plan. Included in the plan were changes to all elementary and middle schools, the high school, the War Memorial

Stadium and the construction of a new aquatic complex. The facilities master plan was estimated at a cost of $187 million.

The original plan for the aquatic complex included a 50-meter and a 25-meter pool, decking, concession area, four rows of bleacher seating, changing rooms, restrooms, equipment space and a solar heating system. The initial estimated cost for the aquatic complex was $10,570,000.

The total budget for all changes to be funded by a bond was over $130 million. An additional amount of $58.2 million was needed for potential repairs and modifications for the schools that would have to be funded. The aquatic complex was included in the proposed bond to improve the high school athletic performance of the swim and water polo teams. The high school currently practices at a municipal pool across town, next to Flamson Middle School. They do not have an adequate venue to conduct swim meets. One of the intentions of the aquatic complex was to improve student access and competitiveness, as well as potentially attracting new students.

These facility changes could only be accomplished through external funding using taxpayer funded bonds. The district modified the wish list for the aquatic complex over the next four months to prioritize projects and to make it acceptable to voters. Several board meetings and planning sessions were held by the administration and board to discuss the size and scope of the projects and the details of the bond measure. Many changes were made. Projects were massaged into an “A” priority and a potential “B” priority list. Notably, the aquatic complex estimate and scope were significantly reduced. What remained in the bond financing, which was approved for the aquatic complex, was a 50-meter pool and the equipment room. The estimate for the change to the aquatic complex in the FMP was reduced from the original $10.5 million to $5.7 million. This is the amount that voters were asked to approve as part of Measure M. The 25-meter pool, pool deck, concession area, bleachers, changing room, solar water heating system and restrooms were left off the aquatic complex bond issue list that was approved by the Board of Trustees. When the description for the bond issue was written in November of that year, however, all of the items on the list were included. The aquatic complex was listed as a community effort with the School District providing limited financing. Donations and potential, though undocumented, agreements with outside parties were to fund the remainder.

Measure M was planned for the November 2016 general election. The taxpayers of the Paso Robles Unified School Facilities Special District, which does not include students from Pleasant Valley or San Miguel School Districts who attend Paso Robles High School, were asked to pay for the improvements with a Bond Measure M fund for $95 million for school construction.

The bond measure was approved on November 8, 2016 with a 57% majority vote. As part of the voters approving the Measure M Bond, the district was required to institute a Citizens Oversight Committee. This committee is charged with reviewing the use of funds sold using Measure M to assure that they are consistent with the language used in the text of the measure. The Board of Trustees approved the committee members in their February 28, 2017 meeting. The committee is required to publish annual audits. Audits for 2016/17 and 2018 are available on their website. Audits have not been completed since 2018. The district has proposed changes to the content and order of the projects anticipated to be funded by Measure M. The total potential value of the bond remains the same.

On April 4, 2017 the board approved a committee including school staff, the bond consultant and a legal team to start the plan for selling and acquiring bond funds. Initially, anticipation notes were going to be used to do preliminary planning before the actual issuing of bonds for all proposed projects. In the June 27, 2017 board meeting, the trustees agreed to hire SIM-BPK Architects for the design and planning of the school refurbishment projects and new aquatic complex. On July 11, the district sold $3 million worth of bonds for preliminary work for the projects. On August 15, 2017, the Chief Business Officer updated the board on the progress of bond sales and the architectural design effort. The architect presented artist’s rendering of the first phase of the work on Measure M projects on October 10, 2017. Included is a rendering of the aquatic complex. The board suspended work on the aquatic complex, objecting to a lack of outside public restrooms, for which no funds were secured. However, this did not preclude the actual purchase of pool components. Keep in mind, that at this point, the project was still not fully funded.

In January of 2018, the district filed an Environmental Impact Report (EIR) with the City of Paso Robles for the aquatic complex. The EIR was the same as the Measure M scope, which was approved by the voters. It included two pools, decking, an equipment room, storage room,

bleachers, coach’s bleachers, a classroom, administrative office, concession space, locker room with outdoor showers and restrooms making this more elaborate than originally projected. This was a significant increase in scope over what had been originally planned.

As of January 23, 2018, the project design was not complete and funding for the complex was not secured. Regardless, on that date, the board approved the purchase and delivery of components for two stainless steel pools for $945,200. The vote was six in favor and one opposed. The price was higher than the Measure M designated cost. These components were delivered and placed in storage containers in August of 2018. At the time of this report, the majority of pool components remain in storage at the high school site.

In February 2018, the superintendent and other district officials posed for pictures in a simulated groundbreaking photo opportunity at the proposed site. The superintendent, at the photo opportunity, stated he could build the complex for $8.2 million dollars (despite the FMP estimate exceeding $10 million) with Measure M Bond funds providing $5.7 million and anticipating $2.5 million coming from donations. He claimed to have an agreement for the ground clearing, excavation, and site work to be completed by a retired earthwork contractor and winery owner. That agreement was never documented and the party who made the agreement has since passed away.

A group of citizens formed a non-profit organization to raise funds for the donations. SWIMPASO raised several thousand dollars through fundraising efforts. Their contributions were transferred to the 4A Foundation, a group used to fund extracurricular activities at the schools, designated for the construction of the aquatic complex. As of the date of this report there has not been an audit of those funds ($144,473.95) nor any indication of expenditures by the group to support the completion of the aquatic complex.

On March 13, 2018, the Board of Trustees appointed new members of the Measure M oversight committee. The Board was given an update on the progress of the work for rebuilding the schools and the aquatic complex. On April 24, 2018, the Board agreed to sell $40 million dollars of bonds for Measure M repairs and the aquatic complex. The $3 million of anticipation notes previously issued were paid off.

In the ensuing eight months up to November of 2018, the District began physical work. They eliminated temporary structures and leveled the site in preparation for the pool installation. Total expenditures, including the pool components purchased, at that time were $1,308,128. On November 3, 2018, the District presented an update of the Facilities Master Plan including the aquatic complex. The District entertained bidding for the installation of the pools at that time. The bids received from two contractors came in at $11 million and $12.7 million (in addition to the cost of the pool components) and was announced at a January 2019 Board of Trustee meeting. They were substantially over the original estimate and the remaining bond funding set aside for the aquatic complex. The Board voted at that time to put a hold on the project until additional funding could be secured.

Since that time, District staff toured a similar aquatic complex site in Hollister, California. The staff learned that the operating costs for a similar site were substantially more than what was projected for Paso Robles. The manufacturer has recalled one of the pool liners for another similar project and continues to honor a three-year warranty effective when the pool is installed. The last Board of Trustees discussion concerning the Aquatic Complex was at the January 25, 2020 board meeting. The district trustees remained committed to complete the installation that is needed for the high school. They hoped funding could come from a proposed School Modernization Bond, State Measure Proposition 13, in the 2020 primary election. That potential funding source was eliminated by the defeat of the proposition.

CONCLUSION

The Paso Robles School Board of Trustees and the previous superintendent prematurely purchased pool components and committed to an aquatic complex without a fully developed plan and a way to pay for it. It was mistakenly assumed that the additional funding required would be forthcoming. No written agreements have been found that could prove that the needed donations were in place to consummate the building of the complex. As a result of the trustees’ actions, Measure M, as

authorized by the voters, has funded expenses of $1.5 million for an aquatic complex, which is unlikely to be realized. This includes almost a million dollars-worth of pool components, which require additional funding to maintain while stored in metal containers, potentially degrading.

FINDINGS

CHAPTER 1-SCHOOL DISTRICT LEADERSHIP

F1. Budget forecasting errors and mismanaged spending by the administration, without adequate oversight by the board, were compounded over a minimum of three years, leading to a reduction of the district reserves below mandatory minimums.

F2. The superintendent and his staff provided financial information to trustees that was neither accurate nor conducive to making sound financial decisions.

F3. Based on state guidelines for allowable administrative budgets the 25.9 new positions added between 2015 and 2018 exceeded recommended levels and was a key contributor to the depletion of reserves.

F4. Conflict of interest, nepotism, and cronyism, real or imagined, created distrust and suspicion. This also led to teacher morale issues as documented in two union-sponsored surveys.

F5. The superintendent was not eligible for a severance package when he resigned. However, the board extended a negotiated settlement without obligation to do so.

F6. The majority of trustees failed to independently verify information provided to them prior to approving expenses.

F7. Issues exist with the way trustees are prepared for their duties. Not all trustees take advantage of training opportunities to enhance their understanding of complex issues in school management and administration.

F8. The County Office of Education’s ability to intervene in a timely manner is unduly limited. The County Superintendent’s inability to respond resulted in serious budgeting errors over the period of the 2016-2018.

CHAPTER 2-THE DISTRICT RESERVES

F1. Excessive mismanagement and questionable decision making should have been increasingly evident within the PRJUSD during the time period 2015 through 2018.

F2. As a body, the trustees abdicated their responsibility for providing adequate financial oversight.

F3. The Board of Trustees should be expected to attend financial training for the school district. The public should be aware that state law prohibits making this training a requirement.

F4. The instability of staffing because of the rapid turnover of senior staff in the finance office resulted in poor management of district assets.

F5. Significant safeguards within the QSS were circumvented by failure to activate them which ultimately minimized effective budget oversight.

F6. A proper system of checks and balances was not evident during the superintendent’s tenure (2014-2018). The Board of Trustees, as a body, followed the direction of the superintendent, most often without dissent.

F7. The superintendent’s vision and his ability to deliver it, in a fiscally responsible way, appears to have been beyond his skill set resulting in a significant reduction of the district’s financial reserves.

F8. While QSS provides an adequate day-to-day financial management tool, it does not provide adequate reporting capabilities required by the Board of Trustees. Additional tools are needed so that the Trustees can properly provide financial oversight in the best interest of the school district.

CHAPTER 3-THE AQUATIC COMPLEX

F1. The modular pool components were prematurely purchased before the aquatic complex project was fully developed or funded.

F2. A site visit to an existing installation was not conducted prior to purchasing pool equipment constituting a failure of due diligence by the district superintendent and trustees.

F3. It was poor business policy to not have documented proposed donations between the district and donors to fund portions of construction.

F4. The anticipated financial support to complete the project has not materialized, as evidenced by the lack of support for SWIMPASO and 4A Foundation fundraising efforts. Strong community support is not evident.

F5. The Trustees and the superintendent understood Measure M Bond funding allocation was inadequate to complete the aquatic complex. As of the date of this report, the board has chosen not to prioritize the aquatic complex and shift additional bond funding.

F6. Annual operating costs were dramatically underestimated in the planning of the aquatics complex.

F7. The advisory council is negligent in their charge with overseeing the execution of Measure M Bond funds and has not published an audit for two years as required by the measure.

F8. The Board of Trustees did not use due diligence and failed in their fiduciary obligation to properly complete the aquatic complex, lacking a reasonable design, construction and financial plan before purchases were approved.

RECOMMENDATIONS

R1. District policy should be amended to prevent a school district superintendent from acting simultaneously as CBO.

R2. The District shall require comprehensive training for new hires who are responsible for financial accounting and business operations.

R3. The structure for board meetings should be revamped to provide a more reasonable and focused agenda. Targeting the focus of each meeting would allow effective action and increased accountability by trustees.

R4. In order to maintain institutional history and knowledge, the district should develop a succession plan to ensure timely replacements for essential positions and time for appropriate training.

R5. Both the School District and the District Board of Trustees Procedure Manuals should be reviewed and updated annually and made readily available on the district website.

R6. By-laws should be amended so that all trustees are encouraged to participate in comprehensive training with emphasis on financial oversight as provided by SLOCOE and other sources.

R7. The County Office of Education should revisit its policies to provide further clarification on conflict of interest. All employees and board members shall be required to disclose any potential conflict issues.

R8. The Chief Business Officer should have the authority to independently report on the fiscal health of the school district to the Board of Trustees and the County Board of Education.

R9. The County Board of Education should provide tighter controls and transparency over authorizations for overriding a school district’s approved budgets.

R10. Prior to an election, school districts should publicize the financial responsibility of the Board of Trustees to facilitate the complex scope of their fiduciary duties if elected.

R11. Trustees must establish and document standard minimum qualifications for a superintendent, which reflect the needs of the district including financial management.

R12. Standardized financial and performance metrics and monthly reporting should be developed to provide the board of trustees with the tools necessary for effective decision- making and greater accountability related to specific goals and financial objectives.

R13. Under the conditions that exist today, the district trustees and administration should determine if the aquatic complex is viable.

R14. The PRJUSD should consider the possibility of collaborating with the city of Paso Robles to use purchased equipment to upgrade current municipal swim facilities.

R15. There should be a comprehensive audit and report made available to the public of 4A Foundation funds that were dedicated to the aquatic complex construction.

R16. There should be a current audit of Measure M Funds by the Oversight Committee and it should be made available to the public.

REQUIRED RESPONSES

The Superintendent of Paso Robles Joint Unified School District shall respond to Recommendations 1, 2, 3, 4, 5, 8, 12, 13, 15, and 16.

The Board of Trustees for the Paso Robles Joint Unified School District shall respond to Recommendations 1, 2, 3, 4, 5, 6, 8, 10, 11, 12, 13, 14, 15, and 16.

San Luis Obispo County Office of Education Superintendent shall respond to Recommendation 7, 8, 9, and 10.

City Manager for the Paso Robles City Council shall respond to Recommendation 14.

The responses shall be submitted to the Presiding Judge of the San Luis County Superior Court, Judge Duffy, by February 17, 2021. Please provide a paper copy and an electronic version of all responses to the Grand Jury.

AGENCY RESPONSE REQUIREMENTS

The Penal Code Section 933.05 that specifies the format and methodology for agency responses is listed below. All agency respondents are required to respond to all findings and recommendations in the following manner:

• If the respondent disagrees wholly or partially with an item, the respondent must elaborate on the portion of the item that they disagree with, and provide an explanation.

• If a respondent notes that an item will be implemented in the future, the response must include a timeframe for implementation.

• If a respondent notes that an item requires further analysis, the agency must include in the response an explanation of and the scope of what will be studied and the timeframe needed for the study. The timeframe for follow-up from the agency cannot exceed six months.

• If the item will not be implemented or is not reasonable, the respondent is required to provide a detailed explanation.

933.05. Findings and Recommendations

(a) For purposes of subdivision (b) of Section 933, as to each grand jury finding, the responding person or entity shall indicate one of the following:

(1) The respondent agrees with the finding.

(2) The respondent disagrees wholly or partially with the finding, in which case the response shall specify the portion of the finding that disputed and shall include an explanation of the reasons therefore.

(b) For purposes of subdivision (b) of Section 9ss, as to each grand jury recommendation, the responding person or entity shall report one of the following actions:

(1) The recommendation has been implemented, with a summary regarding the implemented action.

(2) The recommendation has not yet been implemented, but will be implemented in the future, with a timeframe for implementation.

(3) The recommendation requires further analysis, with an explanation and the scope and parameters of an analysis or study, and a timeframe for the matter to be prepared for discussion by the officer or head of the agency or department being investigated or reviewed, including the governing body of the public agency when applicable. This timeframe shall not exceed six months from the date of publication of the grand jury report.

(4) The recommendation will not be implemented because it is not warranted or is not reasonable, with an explanation therefore.

APPENDIX A

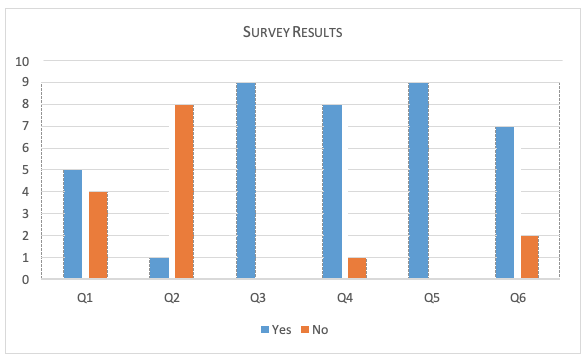

Results of the Grand Jury Survey of the Ten Primary SLO School Districts Survey Questions For Superintendents:

1. Does your district provide budgetary/financial management training for school board members?

2. Is the training mandatory?

3. Do your school board members have specific documented responsibilities and authorizations?

4. Does your district provide documented rules or guidelines for school board trustees?

5. Does your district require specific qualifications or training for the district superintendent?

6. Does the district require specific qualifications or training for the CBO?

Survey Results From Superintendents:

Summary of responses:

Nine of the ten SLO school districts replied to this survey. As indicated in the graph, at least half of the districts provide some form of fiscal management training to trustees, but only one of the five districts who train make it mandatory. Many indicated in the comments that trustees are encouraged and subsidized to attend professional conferences and workshops available through the California School Board Association as well as other organizations. All the nine respondents indicate some form of written policy on the authorizations and responsibilities of trustees, and eight of the nine indicate they have documented guidelines in place for them. Those guidelines are in the form of by-laws, policies and job descriptions, though one district admitted that the district only makes these available to trustees and does not provide a copy to each directly. As for qualifications and training for superintendents, all nine districts have delineated qualifications, one specifically indicated that a doctoral degree is expected of all candidates. In the additional comments some of the districts said they support professional development and it is written into at least one superintendent’s contract as a requirement. As for the Chief Financial Officer, two districts have a Superintendent/CBO combo position due to the smaller size of the district. In one of those cases they contract with the County Office of Education for business services including the production of all financial reports. Seven districts indicate that they have qualifications spelled out for CBOs, one saying that FCMAT (Financial Crisis and Management Assistance Team) Certification or equivalent is required for the position.